Shadow Banking System: -(Understanding Finance Beyond Banks)

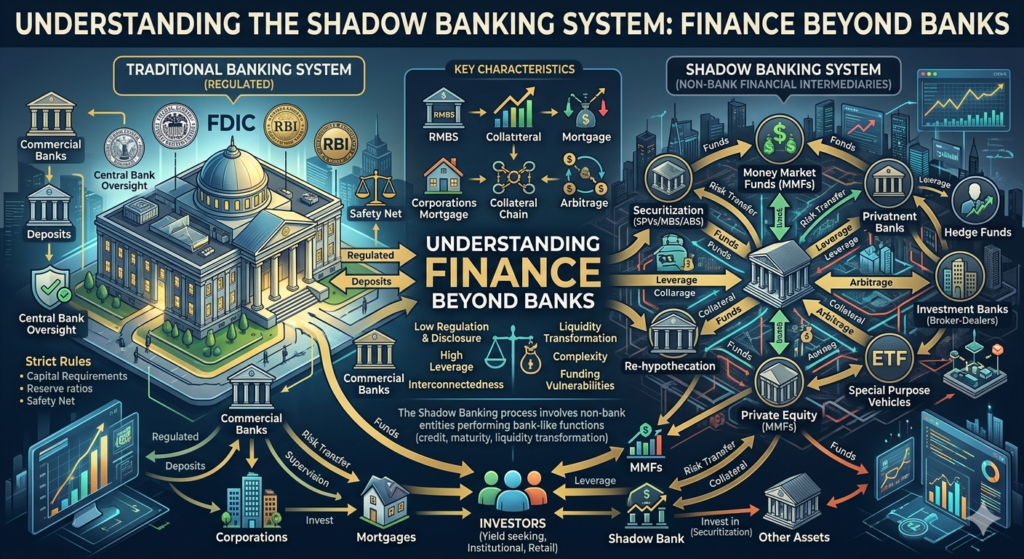

When people think about finance, banks are usually the first institutions that come to mind. Banks accept deposits, provide loans, and work under strict rules set by regulators. However, the modern financial system is much wider than just banks. Alongside the formal banking sector, there exists another layer of institutions that also provide credit and liquidity but do not operate as traditional banks. This parallel arrangement is known as the shadow banking system.

The term “shadow” can sound misleading. It does not mean that these activities are illegal or hidden. Instead, it refers to financial institutions and practices that operate outside the conventional banking framework. Over time, shadow banking has become an important source of finance for businesses, households, and even governments, making it a significant part of the overall financial system.

What Is the Shadow Banking System???

In simple words, the shadow banking system includes all those financial entities that perform bank-like functions without being banks. These institutions do not take deposits from the public in the usual sense, but they still mobilise funds and lend money.

Some basic features help define this system clearly:-

It does not rely on regular savings or current accounts.

Funding mainly comes from markets or investors.

Regulatory control is lighter compared to banks.

Operations are closely linked with financial markets.

Because of these characteristics, shadow banking works parallel to the formal banking system while remaining connected to it.

Institutions That Form the Shadow Banking Network

Shadow banking is not a single organisation. It is a collection of different financial entities, each playing a specific role in credit creation.

Important participants include:-

Non-Banking Financial Companies (NBFCs) that provide loans, leasing, and asset finance.

Money market and investment funds that collect funds from investors and lend them further.

Hedge funds and private investment funds that operate with higher risk and leverage.

Securitisation vehicles that convert loans into marketable securities.

Together, these institutions create an alternative channel of finance outside traditional banking.

Why Did Shadow Banking Grow So Rapidly?????

The expansion of shadow banking is closely linked to changes in the formal banking system. As banking regulations became stricter, alternative sources of credit gained importance.

Some key reasons for its growth are:-

Higher capital and compliance requirements for banks.

Demand for quicker and more flexible credit.

Growth of financial markets and new instruments

Investors searching for better returns.

Shadow banking emerged as a response to these economic and regulatory conditions.

How Shadow Banking Creates Credit

Unlike banks, shadow banking institutions depend largely on market-based finance. They raise funds from investors rather than depositors.

The usual process works like this:-

Funds are collected from markets or investors.

Loans are given to businesses or individuals.

In some cases, loans are bundled and sold as securities.

Returns come from interest payments and asset values.

This system allows money to move faster, but it also increases dependence on market confidence.

Contribution to the Economy:-

Shadow banking plays an important role in supporting economic activity. It often complements the formal banking system rather than competing with it.

Its major contributions include:-

Better access to credit for small and medium enterprises.

Support to sectors where banks are cautious.

Encouragement of financial innovation.

Diversification of credit sources.

In many economies, shadow banking helps bridge gaps left by traditional banks.

Risks Linked to Shadow Banking:-

Despite its benefits, shadow banking carries serious risks. These risks mainly arise because of lower regulation and strong market dependence.

Major concerns include:-

Liquidity mismatch between short-term funding and long-term lending.

High levels of borrowing that increase vulnerability.

Limited transparency in complex financial structures.

Strong interlinkages with the formal banking system.

During economic stress, these weaknesses can amplify financial instability.

Shadow Banking and Financial Crises:-

Past financial crises have shown that shadow banking can transmit shocks very quickly. When investors lose confidence, funding dries up almost instantly.

Such situations highlight:-

Fragility of market-based funding.

Speed at which panic spreads.

Spillover effects on banks and the real economy.

These experiences changed how policymakers view non-bank financial activities.

Regulation:-( Finding the Right Balance)

Regulating shadow banking is challenging. Excessive regulation can restrict innovation, while weak oversight can increase risk.

Regulatory efforts generally focus on:-

Improving transparency and disclosure.

Monitoring leverage and liquidity risks.

Limiting excessive risk-taking.

Strengthening indirect supervision.

The aim is to reduce risk without blocking credit flow.

Role in Developing Economies:-

In developing economies, shadow banking plays a different but important role. Formal banks may not reach all sections of society.

Shadow banking supports:-

Small businesses and informal sectors.

Housing and infrastructure financing.

Alternative credit needs.

However, rapid growth without proper oversight can increase financial vulnerability.

Technology and the Future of Shadow Banking:-

Digital platforms and financial technology are changing the nature of shadow banking. Online lending and data-driven credit assessment are expanding rapidly.

Future developments may include:-

Greater use of digital lending platforms.

Closer regulatory monitoring.

Blurring boundaries between banks and non-banks.

Technology will shape how shadow banking evolves in the coming years.

Conclusion:-

The shadow banking system is an important but complex part of modern finance. It improves access to credit, supports innovation, and complements traditional banks. At the same time, it creates risks related to liquidity, leverage, and financial stability. The real challenge lies in recognising its importance while managing its weaknesses. A balanced approach that encourages transparency and responsible growth can ensure that shadow banking supports economic development without creating systemic instability.